Roof Repair Depreciation Life

What Is The Depreciation Of The Roof On A Commercial Building

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Part Three The Value Of Accurate Roof Age In Claims

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

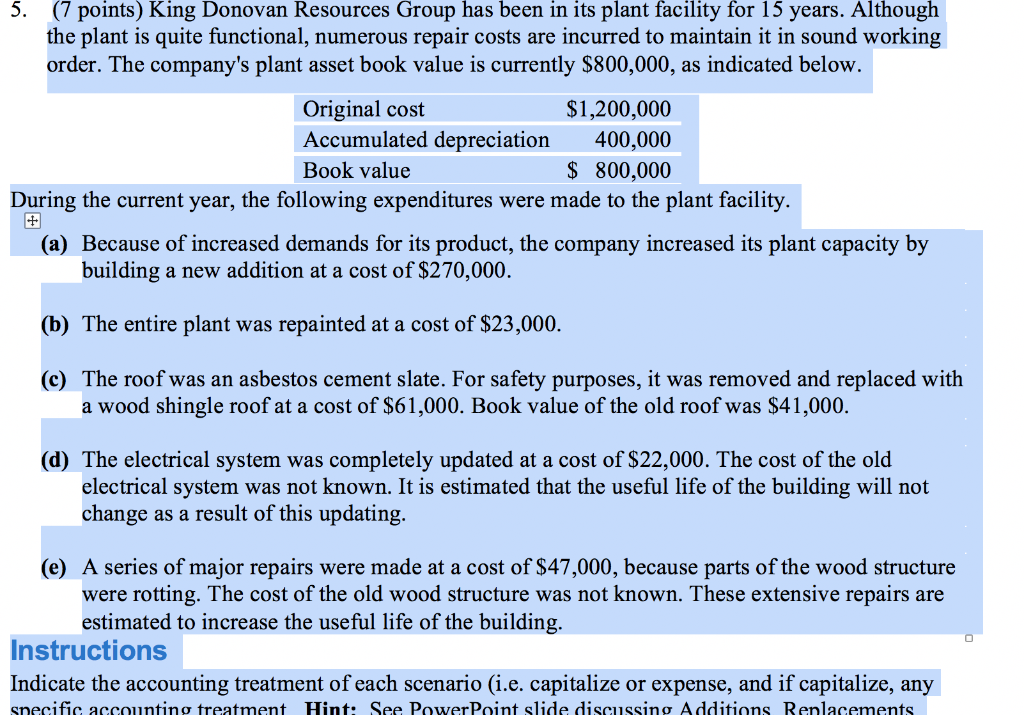

Solved 7 Points King Donovan Resources Group Has Been I Chegg Com

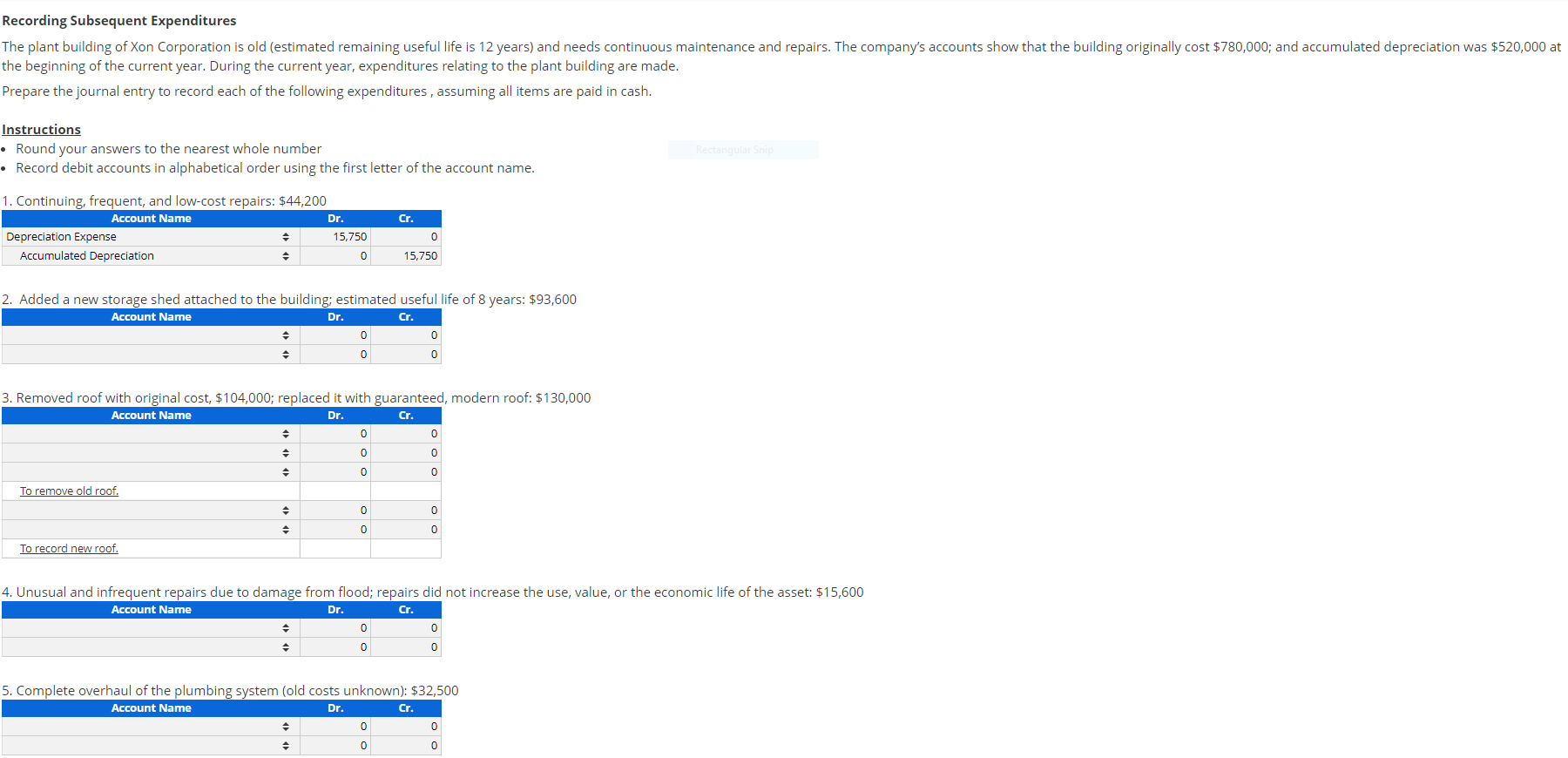

Recording Subsequent Expenditures The Plant Buildi Chegg Com

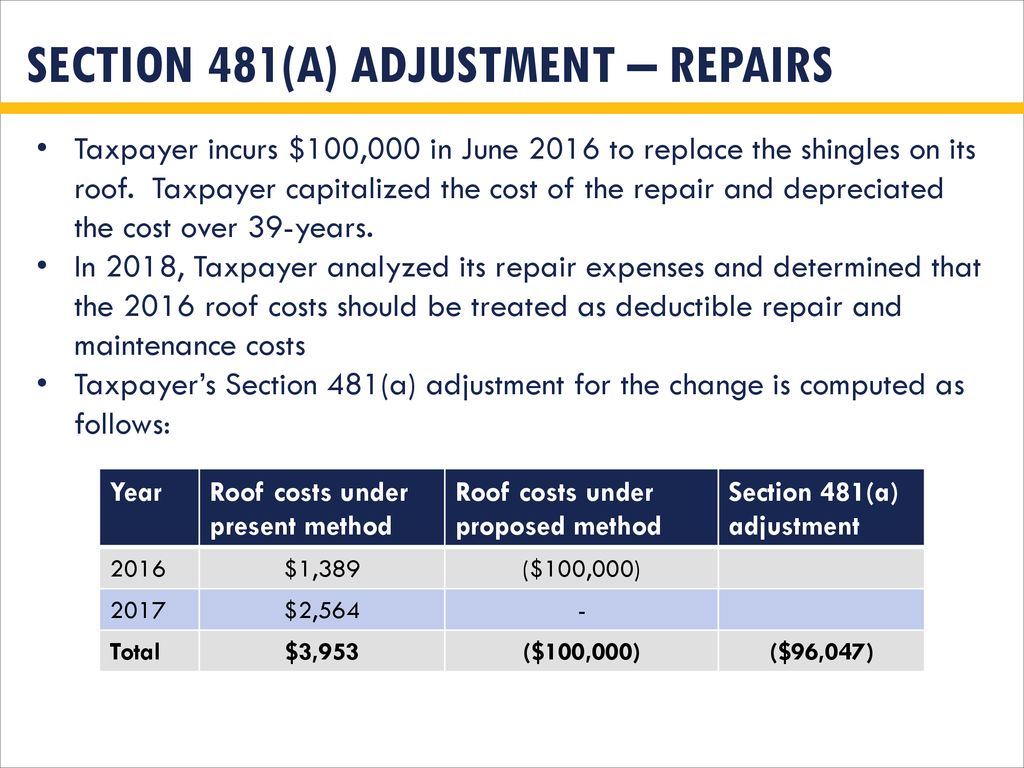

Improvements are depreciated using the straight line method which means that you must deduct the same amount every year over the useful life of the roof.

Roof repair depreciation life. The recoverable depreciation also happens to be 5 000 10 000 replacement value less 5 000 actual cash value. Complex irs regulations give owners of apartment buildings and other commercial structures two options when they dispose of a building s structural components such as a roof hvac unit or windows. The most common and often significant item that is evaluated is roofing related work. If you classify it as an improvement you have to depreciate it over 27 5 years and you ll get only a 350 deduction this year.

For the first time the section 179 internal revenue code allows building owners to expense the cost of a new roof in 1 year instead of spreading it out over 39 years. In many cases only a portion of the roofing system is replaced and depending on the facts those costs may be deducted as repairs. Unfortunately telling the difference between a repair and an improvement can be difficult. The irs designates a useful life of 27 5 years so divide the total cost of the roof by 27 5 to reach the amount you are able to deduct each year.

Repainting the exterior of your residential rental property. Let s say your roof is supposed to last 20 years and it s 5 years old when damaged. For example going from asphalt shingles 20 year life to clay tile 50 year life is a betterment that requires capitalization. They can either continue to depreciate the cost of the replaced component or they can fully deduct the unrecovered cost of the component in the year it is replaced.

The irs states that a new roof will depreciate over the course of 27 5 years for residential buildings and over the course of 39 years for commercial buildings. That s a big difference. The roof depreciates in value 5 for every year or 25 in this case. Each year tax professionals who deal with real estate must evaluate the most recent building expenditures and determine which items should be written off as a repair expense or capitalized.

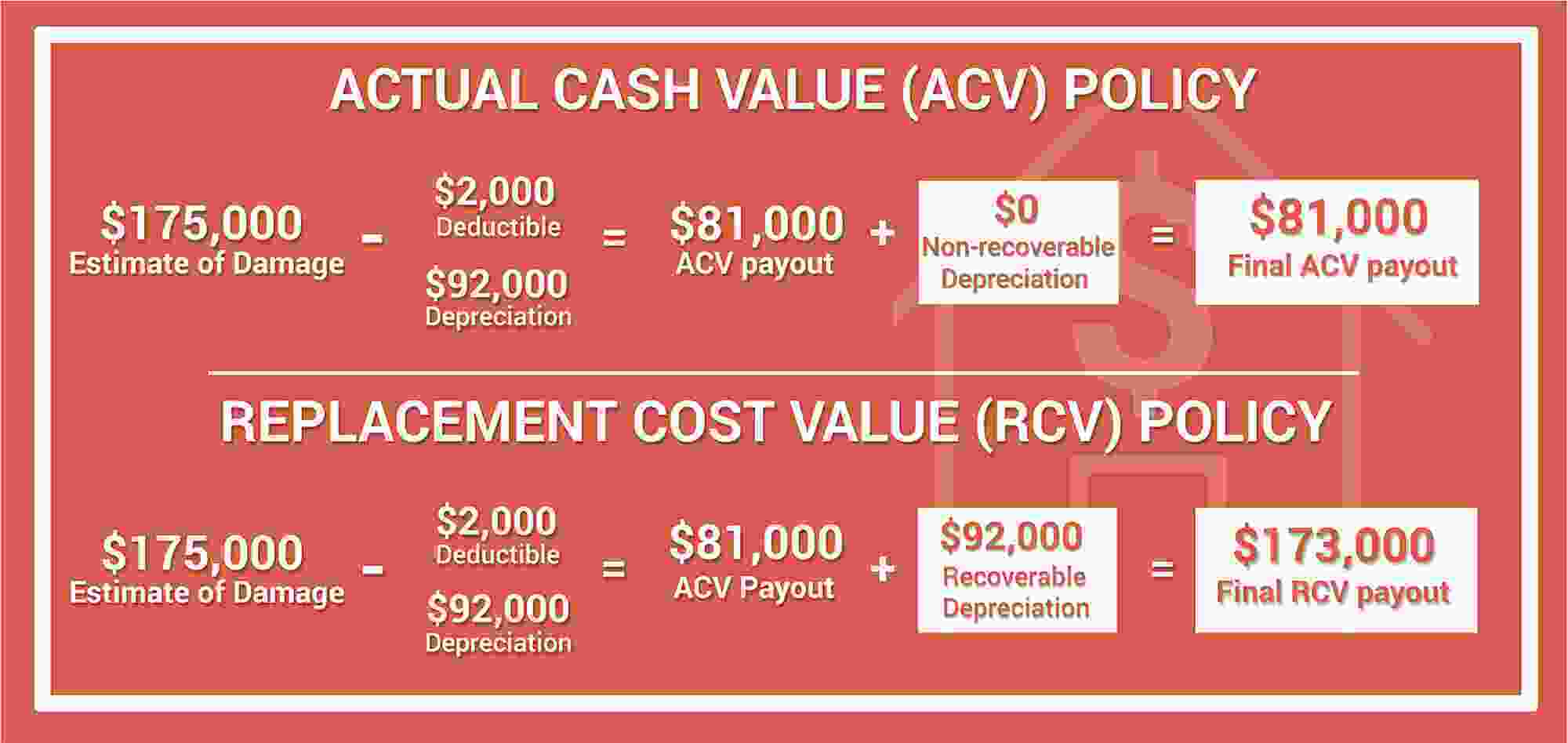

The insurance adjuster depreciated the roof 50 an arbitrary number based on its age so the actual cash value of the roof is now 5 000. By stephen fishman j d. The irs uses the straight line method to calculate the depreciation of your roof which means that the depreciation of your roof is calculated evenly across a set period of time. The full replacement cost of the roof is 10 000.

When a claims adjuster looks at a roof he will consider the condition of the roof as well as its age. If the roof is in decent condition for its age there may be little to no adjustment for the condition. Are generally depreciated over a recovery period of 27 5 years using the straight line method of depreciation and a mid month convention as residential rental property.

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin Insurance Deductible Home Insurance Insurance Marketing

Rcv Vs Acv Whats The Difference A Young Insurance Agency Inc

Https Www Calt Iastate Edu System Files Premium Video Files Rr 20dispositions 20 203 20per 20page Pdf

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

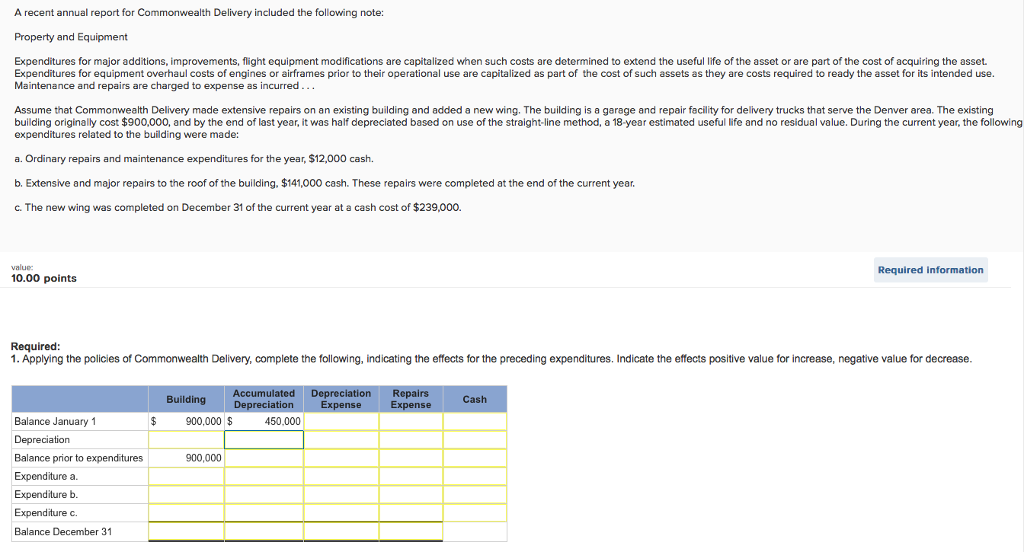

Solved A Recent Annual Report For Commonwealth Delivery I Chegg Com

Rental Property Depreciation Rules Schedule Recapture

How The New Tax Law Affects Rental Real Estate Owners

Depreciating Labor Costs The Rough Notes Company Inc

Homeowners Insurance 101 Roof Age Matters At Claim Time

179 Tax Deduction For Commercial Roofing Projects Advanced Roofing Inc

Can I Make Money Off My Insurance Roofing Claim Slade Roofing

Recapitalization Capital Renewal What S The Number Tradeline Inc

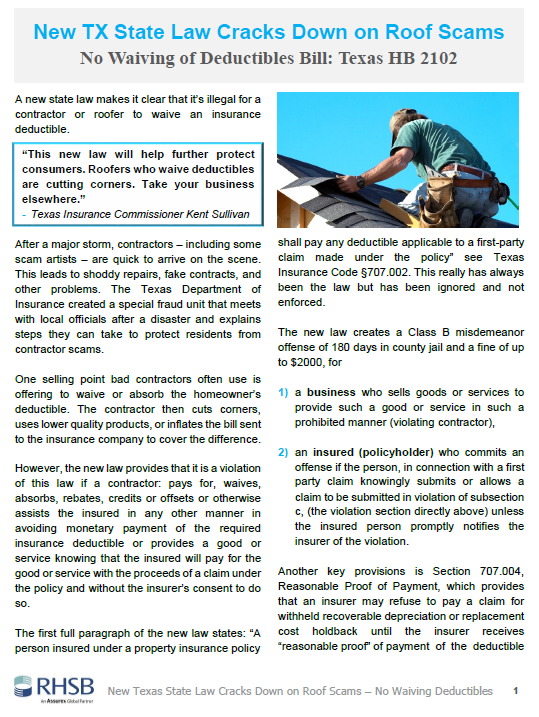

New Tx State Law Cracks Down On Roof Scams No Waiving Deductibles Rhsb

Accounting Method Changes Post Tax Reform Ppt Download

Pin Di Destinasi

Roof Insurance Acv Vs Replacement Cost Bankrate

How To Get Insurance To Pay For Roof Replacement Rgb Construction

Guide To Expensing Roofing Costs Expense Vs Capitalized Bergankdv

Overview Of The Cost Approach Final Reconciliation Ppt Download

Section 179d Tax Deduction For Commercial Roof Replacements

Hospitality Capex Math 101 Useful Life Cayuga Hospitality Consultants

Roof Insurance Claim Denied

How Long Does A Roof Last Age Of Roof And Insurance Harry Levine

What Residential Roof Warranties Will Cover In Kansas City Pyramid Roofing

The Top 14 Rental Property Tax Deductions Investors Should Know

What Recoverable Depreciation Means And How To Calculate It

What Is Rental Property Depreciation And How Does It Work

Should You Repair Your Roof Or Sell As Is Redfin

Roof Repair A Cost Segregation Case Study Insights Blum

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin

Http Www Slpconsults Com Content Client 9ef9a41463fcf765470c2809ade2e6f8 Uploads Pdf Sfaa 20article 20leanne 20sawyer 20september 202016 Pdf

Depreciable Life Life Expectancy For Rental Purchases

Section 179 Tax Deduction For Commercial Buildings Cleveland Ohio Commercial Roofing Contractor

Replacing Your Roof With An Insurance Claim

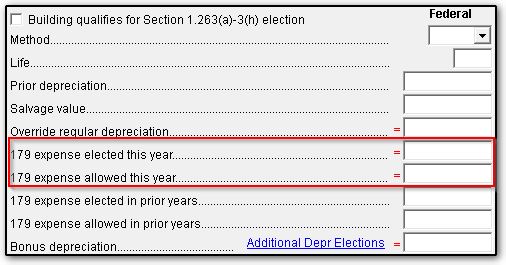

4562 Section 179 Data Entry

Warranties Lifestyle Home Improvement Roofing And Construction Oklahoma City Ok

Cam And Capital Expenses Retail Real Estate Law Ruminations

Insurance Roof Replacement Questions You Should Know

Pin On Articles Tips

Is Roof Replacement Tax Deductible Prime Roofing

Replacement Cost Value Rcv Vs Actual Cash Value Acv

Should You Replace Your Roof After Hail Damage

Roof Replacement Tax Credit Leaffilter